By Quantitative Brokers, October 2017

These days it is hard to imagine there are any investors, investment managers or proprietary traders not focused on minimizing the commissions they pay. Particularly in times when performance is challenged, reducing the amount paid in commissions to the lowest level possible while retaining necessary services is an obvious and common area of focus. However, this is only one part of the total transaction costs for executing futures. All broker commissions, exchange fees and clearing house fees are “explicit costs” (the “pennies”). The other, and most often larger, cost is “implicit” (“pounds”). It is surprising how many sophisticated investors, managers and traders remain in the dark when it comes to the implicit costs of trade execution—especially as they can run into many millions of dollars annually. There is always a choice in how you execute your trades—the difference in these choices is where implicit cost savings can be found.

Implicit cost is also known as execution slippage— the difference between where the market is when the decision to trade was made and the average execution price. This can be driven higher by market volatility and illiquid markets. Poor execution, compounded across thousands of trades a year, can lead to large implicit costs. A significant reduction in slippage can be achieved through careful benchmarking, gathering of data, analysis and trying alternative execution methods.

There will always be implicit costs to trading— minimizing them requires data and analysis. ExecutionalgorithmsandTransaction Cost Analytics (“TCA”) have been widespread in the equity markets for many years, but they are comparatively still underutilized in futures markets. Those who discover the best execution process can find an edge with some discipline and determination. The good news is there is technology available to assist. Once a solution is in place that can give access to regular reports, discipline is needed to regularly review the data with an open mind, and change execution methods when there is evidence doing so will save money.

For some firms, this can be an “ah ha” moment, but getting there requires the ability to question current practices and a willingness to try new execution techniques. TCA can be surprisingly simple once the data has been well organized to make “apples to apples” comparisons.

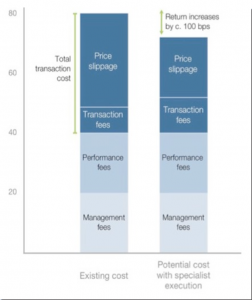

Let’s go through an example of a hedge fund with $1 billion AUM that actively trades futures:

- Let’s suppose four million lots are traded over the course of a year via traditional methods and the fund returns +10%.

- If broker commissions, exchange fees and clearing house fees amount to $2 per lot, explicit transaction fees total $8

- An alternative approach would be to use a “premium” execution algorithm that is an additional explicit cost of $0.75 per This will cause transaction fees to rise by $3 million over the year.

- If using this algorithm drives down the slippage by $3 per lot, annual implicit costs can be reduced by $12 million. This approach produces a net savings of $9 million, improving the return by close to 100 basis points—obviously a substantial difference.

Diagram 1: Real costs of execution for investors theoretical $1 billion portfolio with 10% return after trading 4 million futures contracts

This is the power of understanding total transaction costs and trying alternative execution methods. It is easy to overlook what you can’t see, so instead shine a light on it and potentially save money. The difference in implicit costs could be substantial; in some cases this could equate to management fees or the difference needed to outperform peers. It can be the difference between positive and negative returns. Quite simply, it can be the difference between success and failure.

Quantitative Brokers (QB), an independent, global financial technology company, is a leading provider of advanced algorithms and data-driven analytics to clients in the Futures and US Cash Treasury markets. QB continually develops and innovates an evolving suite of products to reduce implicit trading costs for its clients. QB has offices in New York City, London and Chennai.